Most jewelry owners assume their homeowners policy has them covered. It doesn’t, at least not the way they think. 70% of Americans own jewelry worth over $1,500, yet only 55% insure it properly, and 53% of those who do rely on homeowners insurance without realizing how little it actually pays out. Whether you just received an engagement ring, inherited a family heirloom, or built a collection over years, understanding the real gaps in your coverage could save you thousands of dollars and a lot of heartbreak.

Table of Contents

- What jewelry insurance covers that homeowners policies don’t

- Why your jewelry is at risk: Real theft data and hidden dangers

- Common mistakes: Homeowners claims and why they backfire

- How to get proper jewelry coverage: Steps and best practices

- Who needs jewelry insurance? Real-world examples

- Protect your jewelry investment today with SuperJeweler

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Specialized coverage matters | Homeowners policies are insufficient for high-value jewelry and often leave you exposed. |

| Theft risk is real | Jewelry crime and loss statistics show actual danger, especially for valuable pieces. |

| Standalone policies protect your home | Filing jewelry claims on homeowners insurance can hurt your rates, but jewelry policies prevent this. |

| Appraisals need updates | Get new appraisals every few years to reflect market prices and ensure proper coverage. |

| Peace of mind is affordable | Dedicated jewelry insurance offers robust security and reassurance at a modest cost. |

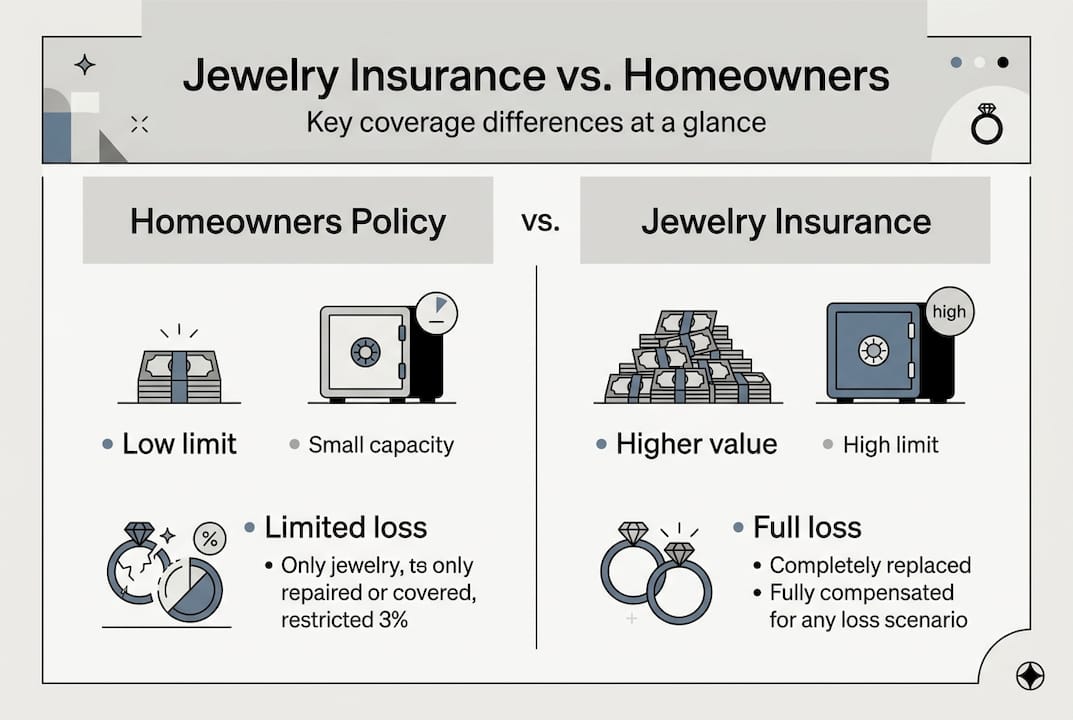

What jewelry insurance covers that homeowners policies don’t

Here’s the part most people miss: homeowners and renters insurance treat jewelry as just another household item. That means your $5,000 diamond ring gets lumped in with your blender and your TV. Standard policies cap jewelry coverage at $1,000 to $2,500, which sounds reasonable until you realize that a single quality engagement ring can cost five to ten times that amount.

Specialty jewelry insurance works completely differently. It’s built specifically for portable, high-value items that travel with you everywhere. These policies offer what’s called “all-risk” coverage, meaning they protect against loss, theft, accidental damage, and even mysterious disappearance, which is when a piece simply vanishes with no explanation. Your homeowners policy almost certainly excludes that last one.

Here’s a quick comparison to make the difference clear:

| Coverage type | Homeowners/renters | Specialty jewelry insurance |

|---|---|---|

| Theft | Yes, up to cap | Yes, full value |

| Accidental damage | Rarely | Yes |

| Mysterious disappearance | No | Yes |

| Coverage cap | $1,000 to $2,500 | Appraised value |

| Deductible | High (often $500+) | Often $0 to $100 |

| Premium impact | Yes | No |

The jewelry insurance value you get from a standalone policy is dramatically higher than what a home policy offers. Think about it this way: if you bought meaningful jewelry gifts for someone you love, wouldn’t you want them fully protected?

Key advantages of specialty jewelry insurance include:

- Worldwide coverage that follows your jewelry wherever you go

- Replacement at current market value, not a depreciated amount

- No deductible or very low deductible options

- No impact on your homeowners policy when you file a claim

- Coverage for travel, including international trips

Why your jewelry is at risk: Real theft data and hidden dangers

Theft isn’t a distant, unlikely scenario. Jewelry theft losses reached $142.5 million in 2024, up 7% from 2023, even though the number of incidents actually dropped. That means criminals are getting smarter and more targeted, going after higher-value pieces with more sophisticated methods.

Rising gold prices are making the problem worse. When gold prices climb, so does the incentive to steal. Elevated gold prices increase uninsured risk for anyone who hasn’t updated their coverage to reflect current market values. A ring appraised at $3,000 three years ago might be worth $4,500 today, and if your policy hasn’t kept up, you’re absorbing that gap yourself.

The risks go beyond theft. Consider these real-world scenarios:

- A ring slips off while swimming at the beach

- A bracelet breaks and a stone falls out during travel

- An earring disappears somewhere between home and a restaurant

- A necklace is lost during a hotel stay

- A piece is damaged in a bag or purse

None of these are covered by a standard homeowners policy. If you’re thinking about the benefits of buying jewelry online or keeping up with fashion jewelry trends, it’s worth knowing that every new piece you add to your collection increases your exposure without proper coverage. And if you’re treating jewelry as a long-term investment, protecting that investment is non-negotiable.

“Jewelry theft losses for US firms reached $142.5 million in 2024, up 7% from 2023, driven by increasingly sophisticated burglaries targeting high-value pieces.”

Common mistakes: Homeowners claims and why they backfire

Let’s say your ring is stolen and you file a claim with your homeowners insurer. You might get a payout, but the consequences don’t stop there. Filing a jewelry claim can raise your premiums or even lead to non-renewal of your policy, and 40% of homeowners have no idea this can happen.

Here’s how the process typically goes wrong:

- You file a claim for a stolen or lost piece of jewelry.

- Your insurer pays out, but only up to the policy cap, often far less than the item’s value.

- Your premium increases at renewal because you now have a claim on your record.

- In some cases, your insurer decides not to renew your policy at all.

- You’re left shopping for new homeowners coverage with a claims history that makes you a higher-risk customer.

A standalone jewelry policy sidesteps all of this. Claims go through a separate insurer, your home policy stays clean, and you don’t risk losing coverage on your house because of a lost necklace. If you’re focused on affordable jewelry shopping, the last thing you want is to pay more for your home insurance because of a jewelry claim.

Pro Tip: Keep your jewelry insurance completely separate from your homeowners policy. Even if your home insurer offers a jewelry rider, a standalone policy almost always gives you better coverage with fewer consequences.

How to get proper jewelry coverage: Steps and best practices

Getting the right coverage isn’t complicated, but it does require a few deliberate steps. Here’s how to do it properly:

- Get a professional appraisal. Every insurable piece needs a written appraisal from a certified gemologist. This document establishes the replacement value your insurer will use.

- Update appraisals every three years. Appraisals must be updated every 3 years to reflect inflation and changes in gold or gemstone prices. An outdated appraisal means you’re underinsured.

- Understand replacement cost vs. actual cash value. Replacement cost pays what it costs to replace the item today. Actual cash value deducts depreciation. Always choose replacement cost.

- Shop standalone jewelry insurers. Companies that specialize in jewelry coverage offer better terms than a homeowners rider.

- Ask the right questions. Find out if the policy covers worldwide travel, what the deductible is, and whether you need to use a specific jeweler for repairs.

- Document everything. Photograph each piece, save receipts, and store appraisals digitally in a secure location.

If you’re buying a diamond, knowing how to verify diamond quality before purchase helps you get an accurate appraisal from the start. The same applies whether you’re buying a natural stone or exploring the lab-grown diamond process. If you’re new to the category, a guide to buying lab-grown diamonds can help you understand what you’re insuring.

Pro Tip: Take a short video walkthrough of your jewelry collection once a year. Store it in cloud storage. If you ever need to file a claim, visual documentation speeds up the process significantly.

Who needs jewelry insurance? Real-world examples

Still on the fence? Let’s get specific. Nearly 40% of collectors have had items stolen or damaged, and jewelry tops the list of collectibles most frequently affected. That’s not a small number.

Here’s who benefits most from dedicated jewelry insurance:

- Engagement ring owners. The average engagement ring costs well above the $1,000 to $2,500 homeowners cap. If you’re following 2026 engagement ring trends, you know prices are climbing.

- Heirloom holders. Inherited pieces often carry sentimental value that far exceeds their market price. Losing one without coverage is irreplaceable in every sense.

- New collectors. Even a modest collection of three or four quality pieces can easily exceed $5,000 in total value.

- Frequent travelers. Every trip is an opportunity for loss, theft, or damage. Specialty policies cover you globally.

- Recent gift recipients. A birthday, anniversary, or holiday gift is often uninsured the moment it’s unwrapped.

“Jewelry tops the list of collectibles most frequently stolen or damaged, with nearly 40% of collectors reporting a loss or damage incident.”

The common thread across all these scenarios is simple: the financial and emotional cost of losing an uninsured piece is almost always higher than the annual premium to protect it.

Protect your jewelry investment today with SuperJeweler

Understanding insurance is step one. Step two is making sure the jewelry you own, or plan to buy, is worth protecting in the first place. At SuperJeweler, we believe every piece should be both beautiful and a smart purchase.

Whether you’re shopping for lab grown diamond engagement ring deals or browsing our full selection of engagement rings, you’ll find high-quality pieces at prices that make sense. And once you’ve found the right piece, you’ll know exactly what you’re insuring and why it matters. Explore everything we offer at SuperJeweler.com and shop with the confidence that comes from knowing your jewelry’s true value.

Frequently asked questions

Is jewelry insurance worth it for inexpensive pieces?

For items under $1,000, your standard homeowners policy may be enough, but for anything with significant monetary or sentimental value, dedicated coverage is worth it for the peace of mind alone.

How often do I need to update my jewelry appraisal?

Most insurers require an updated appraisal every three years to account for inflation, rising gold prices, and changes in gemstone market values.

Will a jewelry claim raise my homeowners insurance premium?

Yes. Filing a jewelry claim on your homeowners policy can raise your premium or trigger non-renewal, which is why a standalone policy is almost always the smarter choice.

What types of losses does specialty jewelry insurance cover?

Most specialty policies cover loss, theft, damage, and mysterious disappearance, which is far broader than what a standard homeowners policy provides.

Are there risks if I rely on my renters insurance for jewelry?

Yes. Renters insurance caps jewelry payouts at $1,000 to $2,500 and typically excludes accidental loss and mysterious disappearance, leaving most valuable pieces significantly underprotected.

Recommended

- Why jewelry makes great gifts: meaningful & timeless

- Why Invest in Fine Jewelry: 15% Market Growth & Value

- Why Invest in Diamond Jewelry: Value, Beauty, and Security

- Why Buy Fashion Jewelry: Smart Style and Value